Difference between 403b and 457

What is the difference between a 403b and a 457?

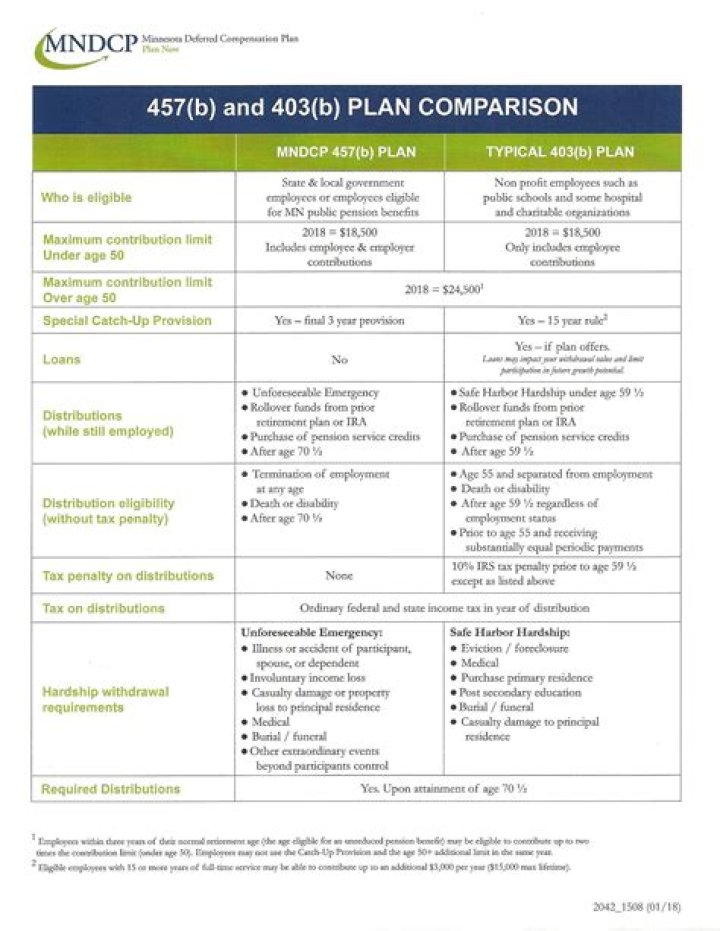

A 457(b) is offered to state and local government employees, while a 457(f) is for top executives in nonprofits. A 403(b) plan is typically offered to employees of private nonprofits and government workers, including public school employees.Can I have a 403b and 457?

Many universities and colleges offer access to both a 403(b) plan and a 457 plan. A question I get often is, “Can I contribute to both a 403(b) and 457 plan?” The answer is yes. If your employer offers both, you can contribute to (and max out) both.How much can you contribute to 403b and 457?

Contributing to both plansGranted, the maximums are pretty high. In 2020, for those under age 50, the annual limit for the 403(b) is $19,500 and $19,500 for the 457. That means you could contribute up to $39,000 combined. That is a huge advantage and one not found in the private sector.

What are 403b and 457 used for?

Similar to 401(k) plans, 403(b) and 457(b) plans allow you to contribute pre-tax money from your paycheck to your 403(b) or 457(b) plan to invest in certain investment products. These pre-tax contributions and their investment earnings will not be taxed until you withdraw the money, typically after you retire.Can you lose money in a 457 plan?

You can take money out of your 457 plan without penalty at any age, although you will have to pay income taxes on any money you withdraw. If you roll your 457 over into an IRA, as many plan holders do, you lose the ability to access the money penalty-free.What happens to my 457 B when I quit?

Once you retire or if you leave your job before retirement, you can withdraw part or all of the funds in your 457(b) plan. All money you take out of the account is taxable as ordinary income in the year it is removed. This increase in taxable income may result in some of your Social Security taxes becoming taxable.How does a 457 plan payout?

The money in a 457(b) grows, tax-deferred over time. When the participant retires and starts to take distributions from their account, those distributions are taxed as regular income. A 457(b) is an example of a defined contribution plan.Is 457 B better than 401k?

Pros and Cons of Saving In a 457(b)One of the main advantages of saving in this type of account is that it’s a non-qualified plan. This means that it’s not subject to the same withdrawal rules as a 401(k). They aren’t technically retirement plans and don’t come with early withdrawals penalties.

Can I use my 457 to buy a house?

When it comes to tapping into the account early, 457(b) plans make it harder to withdraw money in an emergency. “In the 401(k) plan, if you needed money to buy a house or to pay tuition for a dependent, you could do that,” Pizzano says. “But in the 457 plan, those types of foreseeable withdrawals are not allowed.How much tax do you pay on a 457 withdrawal?

5 457(b) Distribution Request form 1 Page 3 Federal tax law requires that most distributions from governmental 457(b) plans that are not directly rolled over to an IRA or other eligible retirement plan be subject to federal income tax withholding at the rate of 20%.Are 457 Plans good?

While there are both pros and cons to choosing a 457(b) retirement savings plan, the pros can tend to outweigh the cons in this case. If you have the ability to contribute to a 457(b), you’re going to enjoy some benefits, like no tax penalties on qualified withdrawals, better catch up provisions, and more.Can I withdraw money from my 457 before retirement?

Money saved in a 457 plan is designed for retirement, but unlike 401(k) and 403(b) plans, you can take a withdrawal from the 457 without penalty before you are 59 and a half years old. There is no penalty for an early withdrawal, but be prepared to pay income tax on any money you withdraw from a 457 plan (at any age).Does a 457 plan required minimum distribution?

If you are a government or non-profit employee, you may have a 457(b). In this case, your savings in this plan can be rolled over, like assets in a 401(k). There is no penalty for early withdrawals but you must take a minimum distribution from age 72.What is the limit for 457 plan?

More details on the retirement plan limits are available from the IRS. The normal contribution limit for elective deferrals to a 457 deferred compensation plan is unchanged at $19,500 in 2021. Employees age 50 or older may contribute up to an additional $6,500 for a total of $26,000.Does 457 reduce taxable income?

457(b) contributions are deducted from your salary before federal, state and local income taxes are withheld (certain exceptions may apply). This means current tax savings are immediate, and reducing taxable income allows you to potentially save more for retirement.Does a 457 count as income?

457 plans are taxed as income similar to a 401(k) or 403(b) when distributions are taken. So if you take the entire amount as a lump sum, the entire amount is added to your income and may push you into a higher tax bracket.Are 457 distributions earned income?

Unfortunately, no this is not earned income.What are the advantages of a 457 plan?

Contributions to a 457 are taken from your gross income, reducing your taxable wages. Your money then grows tax-deferred until you withdraw it, at which point it will be taxed as income. And because, like a 401(k), the deductions are automatic, a 457 offers one of the more painless ways to save for retirement.What are the benefits and disadvantages of a 457 plan?

If you invest in a 457(b) plan, you’ll have access to certain advantages like tax-deferred growth and the opportunity to choose how to invest funds. There are also potential disadvantages to keep in mind, including fees that may be higher than other types of investments and no employer match.Is a 457 better than a Roth IRA?

You Can Max out Both a 457 and a Roth IRAIf tax rates are a lot higher when you retire, you will have significantly benefited from your Roth IRA because your withdrawals are tax-free. If tax rates are lower when you retire, your 457 will have been the more tax-efficient account.